Column: Mind the gap – Brent and WTI point in opposite directions

Brent and WTI prices have diverged sharply in the last month, mostly due to Hurricanes Harvey and Irma which have disrupted refineries, distribution systems and motorists along the US Gulf Coast. Alamy photo.

Brent and WTI gap not expected to last long

By John Kemp

LONDON, Sept 12 (Reuters) – Commuters and tourists are regularly cautioned to “mind the gap” between train doors and the platform at certain stations on the London Underground.

But the warning could just as easily apply to traders in Brent and WTI after the two crude benchmarks diverged sharply over the last month.

Commodity markets abhor a gap and will find a way to arbitrage it away. Such a large gap between forward Brent and WTI prices is unlikely to persist for every long.

Either Brent prices and calendar spreads must weaken, WTI prices and spreads must strengthen, or some combination of both.

In the short term, Hurricanes Harvey and Irma have extensively disrupted oil refineries, distribution systems and motorists along the U.S. Gulf Coast.

The result has been to cut refinery consumption of domestic crude and depress the price of WTI compared with Brent.

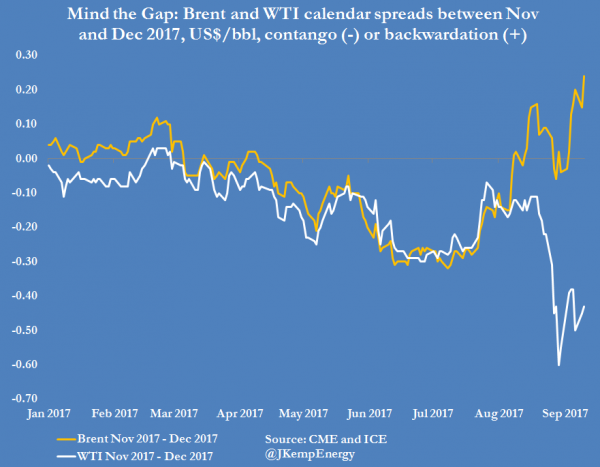

WTI futures for delivery in November 2017 are trading at a discount to Brent of around $5.30 per barrel compared with $2.75 on Aug 14.

WTI is trading in a contango of about 44 cents per barrel between November 2017 and December 2017 compared with a backwardation of 22 cents in Brent.

WTI is trading in a contango of about 44 cents per barrel between November 2017 and December 2017 compared with a backwardation of 22 cents in Brent.

Backwardation in Brent is consistent with a tightening global oil market while contango in WTI is consistent with local oversupply of crude as a result of refinery shutdowns and the closure of export terminals.

Backwardation in Brent is consistent with a tightening global oil market while contango in WTI is consistent with local oversupply of crude as a result of refinery shutdowns and the closure of export terminals.

Most of this can be put down to temporary disruptions caused by the hurricanes.

Restarting refineries after flooding is a slow and complicated process plagued with safety risks (“After Harvey: precautions needed during oil and chemical facility start up“, U.S. Chemical Safety Board, Aug 2017).

Restarting refineries after flooding is a slow and complicated process plagued with safety risks (“After Harvey: precautions needed during oil and chemical facility start up“, U.S. Chemical Safety Board, Aug 2017).

And U.S. export terminals were badly affected by the storm which cut crude exports to just 153,000 barrels per day in the week ending on Sept.1 compared with 902,000 bpd the week before.

So the hurricanes will almost certainly leave the United States with a short-term build up of crude stocks that could linger for some weeks or months until it can be exported or absorbed by domestic refineries.

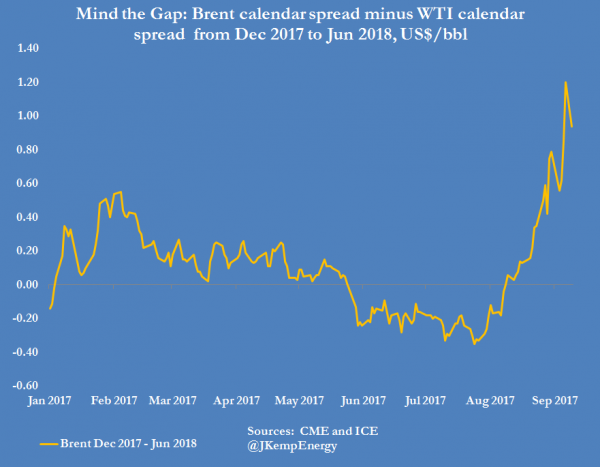

The problem is that the gap extends well into the first half of 2018 when U.S. refineries and export terminals should have been back up and running for several months.

WTI for delivery in April 2018 is currently trading at a discount to Brent of $3.80 per barrel, compared with just $2.50 per barrel on Aug. 14.

WTI is in a contango of more than $1 per barrel for the first half of 2018 compared with just 8 cents in Brent.

Brent futures are signalling a relatively tight global oil market next year while WTI points to continued oversupply.

Brent futures are signalling a relatively tight global oil market next year while WTI points to continued oversupply.

However, the gap will create a strong incentive to export surplus crude from the United States to tighter markets in Europe and Asia.

The risk for oil traders is that the forward Brent-WTI spread snaps back violently once U.S. refineries and export terminals become fully operational again.

(Editing by Louise Heavens)

(Editing by Louise Heavens)

John Kemp is a Reuters market analyst. The views expressed are his own.

Subscribe

If you enjoyed this article, subscribe to receive more just like it.