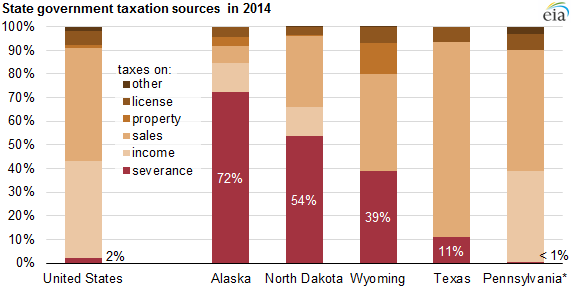

Oil and gas states rely heavily on severance tax

Alaska, North Dakota, Wyoming rely on severance taxes much more than other states

Texas and other states that produce large amounts of fossil fuels rely heavily on severance tax revenue—taxes based on the volume and/or value of oil, natural gas, coal, and other natural resources.

Source: U.S. Census Bureau, 2014 Annual Survey of State Government Tax Collections

Note: Data for Pennsylvania include a wellhead impact fee that was in place instead of a severance tax.

On average, severance taxes accounted for less than 2% of state tax collections in 2014, but in three states—Alaska, North Dakota, and Wyoming—severance taxes provided a much larger share of total state tax revenue in that year.

Pennsylvania, on the other hand, is considering a severance tax, and currently derives less than 1% of its revenues from a well head fee.

Texas. The nation’s largest oil- and natural gas-producing state collected $931 million in severance tax revenues in the first quarter of 2015—more than Wyoming collects in an entire fiscal year. The first-quarter total is down 46% from the $1.7 billion collected in the third quarter of 2014. However, severance taxes cover only 11% of the state operating budget. Texas state and local governments also derive greater oil and natural gas revenues from state land leases and local property taxes. Like Alaska and Wyoming, Texas does not have an individual income tax.

Alaska. Alaska relies on revenues from oil and natural gas production for up to 90% of its budget, and consequently the state experiences fluctuations in tax receipts that reflect changing oil and natural gas prices. The Alaska Clear and Equitable Share Wellhead tax is calculated at 25% of operators’ net income (revenues after operating expenses and capital expenditures) before adjustments and credits. In the first quarter of 2015, the state lost $5 million in severance tax revenues as production companies had negative net income because of falling oil prices and the application of tax credits. Money from Alaska’s Permanent Fund as well as statutory and constitutional budget reserve funds helps the state reduce the effect of year-to-year fluctuations of severance receipts.

North Dakota. The second-largest oil producing state (after Texas) has seen its reliance on severance tax revenues grow along with the growth of tight oil production in the Bakken region. Between 2001 and 2014, North Dakota oil production increased from 87,000 barrels per day (b/d) to 1.1 million b/d, with severance tax receipts over the same period growing from $164.6 million to $3.3 billion. In 2001, severance taxes accounted for 14% of state tax revenues, growing to 54% in 2014. First-quarter 2015 severance tax receipts of $442 million are half of the state’s all-time high of $982 million in the third quarter of 2014. In response to low oil prices, in April 2015 the state passed legislation to revise its severance tax structure, making revenues more predictable. The legislation reduces the oil extraction tax to 5.0% from 6.5% beginning January 2016 and repeals existing statutes that trigger severance tax reductions when oil prices stay below a reference price of $55 per barrel for several months.

Wyoming. The nation’s foremost coal-producing state receives nearly 40% of state revenues from severance taxes. Since 2000, natural gas, rather than coal, has been the largest source of Wyoming severance taxesbecause of a significant increase in natural gas production. High crude oil prices and increases in production elevated crude oil to the second-largest source of severance tax receipts in fiscal year 2014. Wyoming state and local governments also derive revenue from property taxes, with coal, oil, and natural gas totaling more than 50% of state-assessed valuation.

Pennsylvania. Unlike the states discussed above, Pennsylvania, the country’s second-largest natural gas producer, derives revenue not from severance taxes but from an annual wellhead fee based on the number of wellheads drilled and the wholesale prices of natural gas. From 2011 to 2014 the revenues from the impact fees were relatively flat (from $202 million to $226 million) despite production growth in the Marcellus region. This result was because horizontal fracturing techniques yielded increasing natural gas per well and prices remained low. Pennsylvania’s legislature is considering severance tax legislation that would require oil producers to pay a severance tax of 5% of the production value of oil and natural gas. The proposed 5% severance tax is estimated to generate up to $1 billion in tax receipts. This amount would still be less than 3% of the state’s total tax collections because of Pennsylvania’s reliance on other sources of tax revenues.

Subscribe

If you enjoyed this article, subscribe to receive more just like it.