Opinion: US shale booms and depresses oil prices again

The scale of the US shale boom explains why OPEC and its allies are struggling to engineer a deficit in the global oil market and push stocks down to their five-year average. QEP Resources photo.

US shale production expected to rise substantially in 2017, and into 2018

By John Kemp

LONDON, June 1 US oil production continues to rise relentlessly, frustrating efforts by OPEC and non-OPEC oil exporters to rebalance the global market and secure an increase in the price of crude.

After a devastating slump in 2015 and 2016, the US oil industry has returned to strong growth, with drilling and output rising rapidly.

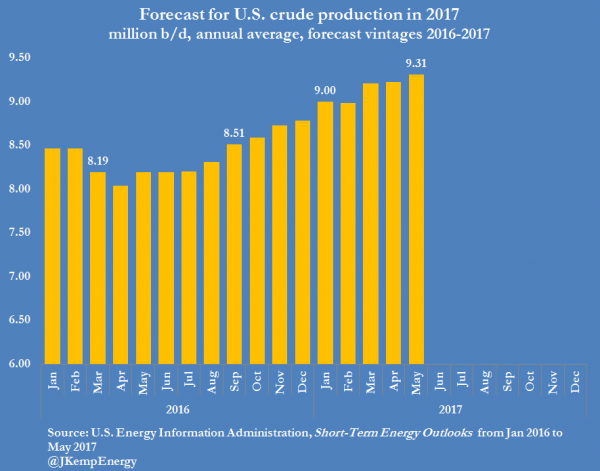

US production is now forecast to grow by an average of 440,000 barrels per day (b/d) in 2017 and another 650,000 bpd in 2018, according to the US Energy Information Administration (EIA).

US production is now forecast to grow by an average of 440,000 barrels per day (b/d) in 2017 and another 650,000 bpd in 2018, according to the US Energy Information Administration (EIA).

US crude and condensates output rose by 62,000 b/d month-on-month to almost 9.1 million b/d in March (“Petroleum Supply Monthly”, EIA, May 2017).

Production has increased by more than 530,000 b/d from its recent low of less than 8.6 million b/d in September, adding to an already well-supplied global market and delaying a drawdown in stocks.

Donate now! Please support quality journalism by contributing to our Patreon campaign. Even $5 a month helps us continue delivering high quality news and analysis about Canadian and American energy stories that affect your life and your lifestyle.

Weekly estimates prepared by the agency indicate output continued to increase in April and May and now stands at around 9.3 million b/d (“Weekly Petroleum Status Report”, EIA, May 19).

While the weekly estimates are considered less reliable than the more comprehensive monthly numbers, they have generally provided a good guide to trends in the monthly data.

Most of the extra output between September and March came from oilfields in the Gulf of Mexico, where production increased by 257,000 b/d, and Alaska, where output was up by 74,000 b/d.

Most of the extra output between September and March came from oilfields in the Gulf of Mexico, where production increased by 257,000 b/d, and Alaska, where output was up by 74,000 b/d.

But production from fields in the Lower 48 states excluding the Gulf of Mexico, most of which comes from onshore shale plays, also rose, by 200,000 b/d.

In March alone, production in the Lower 48 states excluding the Gulf of Mexico rose by 35,000 b/d to its highest level in nearly a year.

In March alone, production in the Lower 48 states excluding the Gulf of Mexico rose by 35,000 b/d to its highest level in nearly a year.

BACK TO BOOM

BACK TO BOOM

US shale output will almost certainly rise substantially in the rest of 2017 and into 2018 given the typical six-month lag between spudding new wells and the beginning of their commercial production.

The number of active oil rigs has now increased to 722, and thousands of extra wells have been drilled in the meantime, with many still waiting on completion services before starting to flow.

As these wells are hydraulically fractured and connected to gathering systems, production will increase further in the remaining months of 2017 and into early 2018.

The speed and scale of the surge in US production has surprised most within the oil industry, even top forecasters.

The EIA predicts US production will hit 9.74 million b/d by the end of 2017 and 10.35 million b/d by the end of 2018 (“Short-Term Energy Outlook”, EIA, May 2017).

As recently as the start of the year, the agency was forecasting output of just 9.22 million b/d by the end of 2017 and 9.44 million b/d by the end of 2018 (“Short-Term Energy Outlook”, EIA, January 2017).

The EIA has revised its predictions for average production in 2017 up by 310,000 b/d and its forecast for the average in 2018 up by 660,000 b/d since January.

With output also rising in Brazil, Norway and several other non-OPEC countries, the scale of the US boom explains why OPEC and its allies are struggling to engineer a deficit in the global oil market and push stocks down to their five-year average.

With output also rising in Brazil, Norway and several other non-OPEC countries, the scale of the US boom explains why OPEC and its allies are struggling to engineer a deficit in the global oil market and push stocks down to their five-year average.

OPEC and non-OPEC are making slow progress despite reported high levels of compliance with output cuts implemented from the start of 2017 and recently extended to the end of March 2018.

Ultimately, prices rather than planned cuts will rebalance the market, which will most likely require a period of flat or lower prices to curb shale growth and ensure US output does not outstrip demand.

(Editing by Dale Hudson)

John Kemp is a Reuters market analyst. The views expressed are his own.

Subscribe

If you enjoyed this article, subscribe to receive more just like it.