US news brief July 12: In disaster’s wake, BP doubles down on deepwater despite surging shale

BP Gulf of Mexico disaster

Also in this brief: US ethanol production continues to grow, Global rig counts all up in June says Baker Hughes

BP’s offshore Gulf Coast development Mad Dog phase two will be profitable even at $40/b oil

Seven years after the disastrous Deepwater Horizon explosion and oil spill in the Gulf of Mexico, BP is spending billions every year to increase production in the area by about 5 per cent annually.

Follow Teo on LinkedIn and Facebook.

“Our strategy is to take this investment that we spent so much money building, and keep it full” to the platform’s capacity, Richard Morrison, BP’s regional president for the Gulf of Mexico, told Reuters during the first tour of a BP Gulf drilling platform since the disaster. “We’re also exploring for larger pools of oil.”

Many of BP’s competitors have switched from offshore investments, which take a lot of time and money, to the quicker returns available through onshore shale plays.

Last month, Anadarko CEO Al Walker told investors “In a $50 to $60 world, we always felt like greenfield development, in the Gulf in particular, was fairly challenged.”

But BP says its Mad Dog phase two, the company’s next Gulf development, will be profitable even at $40/barrel oil. In 2013, BP said it could not start any new deepwater Gulf projects if oil was below $100/barrel.

Drilling innovations, design changes and favourable deals with service providers are helping the company cut costs and increase profits.

BP announced recently that it discovered billions of barrels of oil below its four Gulf platforms. The find is worth more than $40 billion at today’s market prices.

“It seems like every ten years there’s another breakthrough” that unlocks more Gulf oil, Morrison said on the deck of the Thunder Horse, one of the company’s Gulf platforms.

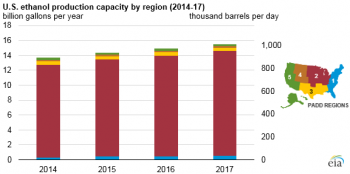

US ethanol production capacity continues to increase

Fuel ethanol production capacity in the United States reached 15.5 billion gallons per year, or 1.01 million b/d, at the beginning of 2017, according to EIA’s most recent U.S. Fuel Ethanol Plant Production Capacity report.

Source: U.S. Energy Information Administration, U.S. Fuel Ethanol Production Plant Capacity

Total capacity of operable ethanol plants increased by about 4 per cent—or by more than 600 million gallons per year—between Jan. 2016 and Jan. 2017.

Most of the 198 ethanol plants in the United States, representing most of the U.S. fuel ethanol production capacity, are located in the Midwest region (as defined by Petroleum Administration for Defense District, or PADD, 2).

Total nameplate capacity in the Midwest was 14.0 billion gallons per year at the beginning of 2017 (918,000 b/d), an increase of about 4 per cent—or by more than 530 million gallons per year—between Jan. 2016 and Jan. 2017.

Nameplate production capacity, the measure of capacity that EIA tracks, is the plant manufacturer’s stated design capacity to produce fuel ethanol during a 12-month period.

Of the top 13 fuel ethanol-producing states, 12 are located in the Midwest. The top three states—Iowa, Nebraska, and Illinois—contain more than half of the nation’s total ethanol production capacity.

In EIA’s June Short-Term Energy Outlook (STEO), U.S. production of fuel ethanol was forecast to reach 15.8 billion gallons (1.03 million b/d) in 2017, equivalent to slightly more than 100% utilization of reported nameplate capacity as of Jan. 1, 2017.

Nameplate capacity is not necessarily a physical production limit for many ethanol plants.

By applying more efficient operating techniques, if market conditions provide an incentive to do so, many ethanol plants can operate at levels that regularly exceed their nameplate production capacity.

This level of operation, called maximum sustainable capacity, is inherently subjective.

Global rig counts all up in June – Baker Hughes

Baker Hughes, a GE company announced the international rig count for June 2017 was 960, up 3 from the 957 counted in May 2017, and up 33 from the 927 counted in June 2016., according to a press release.

The international offshore rig count for June 2017 was 197, down 5 from the 202 counted in May 2017, and down 26 from the 223 counted in June 2016.

The average U.S. rig count for June 2017 was 931, up 38 from the 893 counted in May 2017, and up 514 from the 417 counted in June 2016.

The average Canadian rig count for June 2017 was 150, up 65 from the 85 counted in May 2017, and up 87 from the 63 counted in June 2016.

The worldwide rig count for June 2017 was 2,041, up 106 from the 1,935 counted in May 2017, and up 634 from the 1,407 counted in June 2016.

June 2017 Rig Counts

|

June 2017 |

May 2017 |

June 2016 |

||||||||||||||||||||||||||||

|

Month |

||||||||||||||||||||||||||||||

| Land | Offshore | Total |

Variance |

Land | Offshore | Total | Land | Offshore | Total | |||||||||||||||||||||

| Latin America | 158 | 34 | 192 | 2 | 155 | 35 | 190 | 147 | 31 | 178 | ||||||||||||||||||||

| Europe | 59 | 32 | 91 | -4 | 60 | 35 | 95 | 52 | 39 | 91 | ||||||||||||||||||||

| Africa | 72 | 14 | 86 | 2 | 69 | 15 | 84 | 68 | 19 | 87 | ||||||||||||||||||||

| Middle East | 355 | 42 | 397 | 6 | 350 | 41 | 391 | 341 | 48 | 389 | ||||||||||||||||||||

| Asia Pacific | 119 | 75 | 194 | -3 | 121 | 76 | 197 | 96 | 86 | 182 | ||||||||||||||||||||

| International | 763 | 197 | 960 | 3 | 755 | 202 | 957 | 704 | 223 | 927 | ||||||||||||||||||||

| United States | 909 | 22 | 931 | 38 | 871 | 22 | 893 | 396 | 21 | 417 | ||||||||||||||||||||

| Canada | 148 | 2 | 150 | 65 | 83 | |||||||||||||||||||||||||

Subscribe

If you enjoyed this article, subscribe to receive more just like it.