Rig count more than doubled since last year

By John Kemp

LONDON, May 31 (Reuters) – U.S. exploration and production companies have hired an extra 400 rigs to target oil-bearing formations since the end of May 2016, according to oilfield services company Baker Hughes.

The number of active oil-directed rigs has more than doubled over the last year, from 316 to 722, in one of the most remarkable recoveries on record, coming after one of the deepest slumps during the previous two years.

But the recovery in oil prices has stalled since February and prices are now no higher than they were a year ago. Experience indicates the rig count will stop rising within a few months.

The active rig count is likely to peak in June or July unless the price of benchmark West Texas Intermediate (WTI) crude starts rising again above $50 per barrel.

The active rig count is likely to peak in June or July unless the price of benchmark West Texas Intermediate (WTI) crude starts rising again above $50 per barrel.

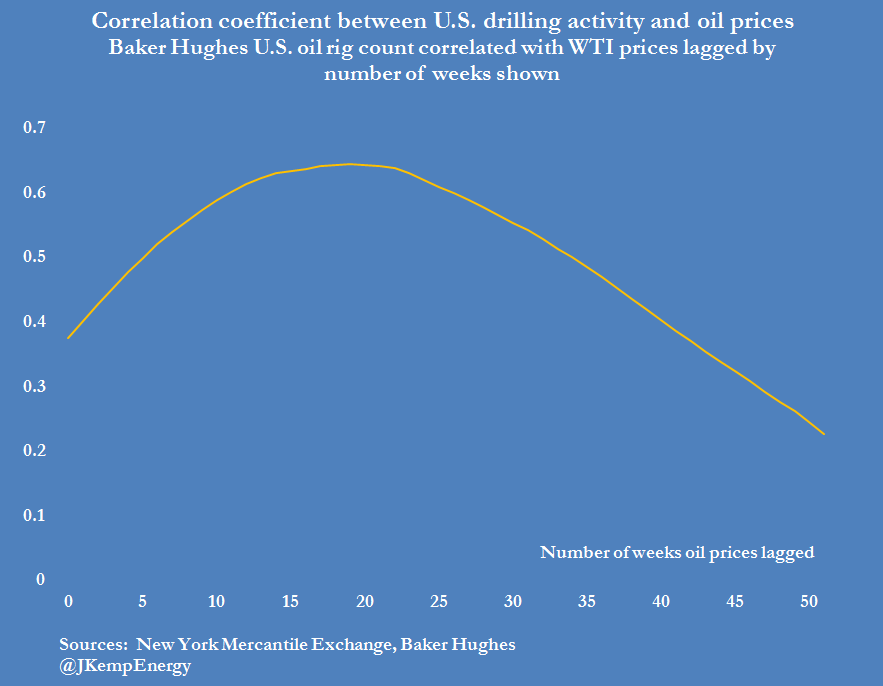

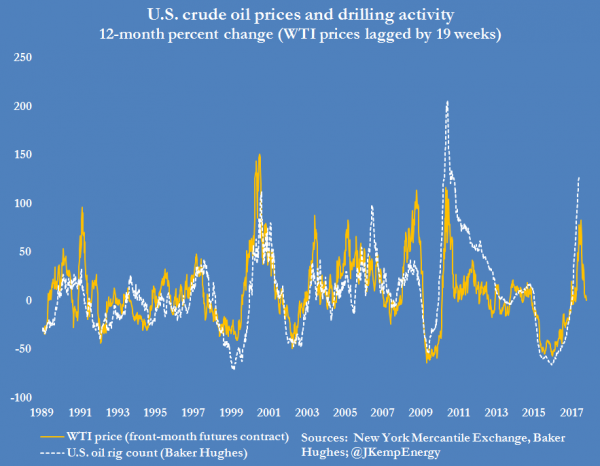

Drilling activity and WTI prices each exhibit a pronounced cycle and are closely correlated.

Price changes typically lead changes in the number of rigs employed, with an average lag of between 16 and 22 weeks.

Price changes typically lead changes in the number of rigs employed, with an average lag of between 16 and 22 weeks.

In 2014, oil prices turned lower in the middle of June and the rig count started to fall 16 weeks later, in mid-October.

In 2014, oil prices turned lower in the middle of June and the rig count started to fall 16 weeks later, in mid-October.

In 2016, prices turned higher from the middle of January and the rig count began to recover 19 weeks later, from the end of May.

But prices stopped rising in late February 2017 and have since drifted sideways or slightly lower, which suggests the rig count is likely to peak between mid-June and the end of July.

But prices stopped rising in late February 2017 and have since drifted sideways or slightly lower, which suggests the rig count is likely to peak between mid-June and the end of July.

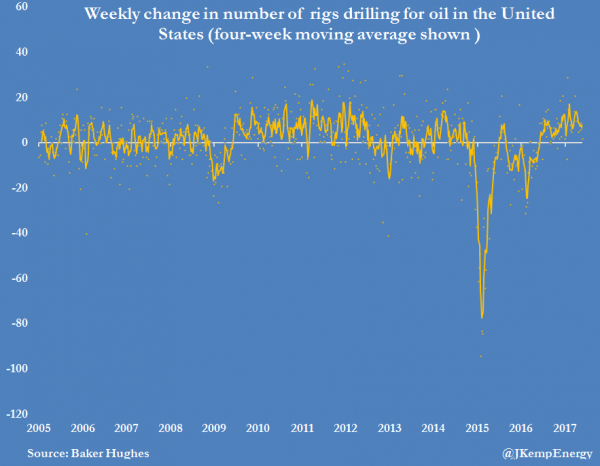

In recent weeks, exploration and production companies have added rigs at a slower pace than earlier in the year, which could be a sign that drilling is already starting to level off.

Baker Hughes BHI.N reports that an average of six oil rigs were added each week in May, down from more than 13 per week in March.

Prominent shale producers have told investors they can drill new oil wells profitably at prices well below the current level of almost $50 a barrel.

Prominent shale producers have told investors they can drill new oil wells profitably at prices well below the current level of almost $50 a barrel.

But further increases in the rig count are likely to require a further increase in prices to make them sufficiently attractive.

The most efficient and powerful rigs have already been called back into service and are drilling on the most productive and low-risk sweet spots in the best shale plays.

If more rigs are added, they are likely to be older, less powerful and less efficient, and will be drilling less productive and riskier wells in areas that are less well known.

Donate now! Please support quality journalism by contributing to our Patreon campaign. Even $5 a month helps us continue delivering high quality news and analysis about Canadian and American energy stories that affect your life and your lifestyle.

The remaining rigs are more likely to remain stacked, or be deployed drilling for gas instead, if prices stay below $50.

However, shale oil production is likely to keep rising through the end of 2017, even if the rig count stabilises in the next few months.

There is an average lag of six months between the spudding of a new well and oil starting to flow (“U.S. oil output poses awkward forecasting problem for OPEC”, Reuters, March 6).

So the resurgence of oil drilling in the second half of 2016 and the first half of 2017 should ensure shale output continues rising into at least the start of 2018.

Drilling costs will also continue rising because they tend to follow changes in the rig count with a lag of two to three months (“Drilling costs rise as U.S. oil and gas activity picks up”, Reuters, April 26).

During the recent downturn, many drilling firms were forced to agree fixed-price contracts that will keep drilling costs contained for much of 2017.

But drilling prices are likely to adjust upwards in late 2017 and through 2018 as those fixed-price contracts expire.

And any extra rigs hired in the second half of 2017 will have to pay higher rates to reflect the strengthening rig market.

Baker Hughes told investors in April it believed the U.S. oilfield services market was “on the cusp of a broader pricing recovery”.

Unless WTI starts appreciating, the combination of higher drilling costs and stalling or lower oil prices is set to moderate the drilling boom and growth in U.S. oil output later in 2017 and especially in 2018.

(Editing by Dale Hudson)

John Kemp is a Reuters market analyst. The views expressed are his own.