Opinion: US drilling costs start to rise as rig count climbs

The increase in drilling costs has begun to reverse the 34 per cent drop reported between March 2014 and November 2016. Nabors photo.

Drilling costs up 8 per cent in June compared to Nov. 2016

By John Kemp

LONDON, July 14 (Reuters) – US oil and gas exploration and production companies are paying more to hire drilling rigs as the number of rigs still idle after the slump declines.

Drilling costs were up by 8 per cent in June 2017 compared with their recent low in November 2016, according to preliminary data from the U.S. Bureau of Labor Statistics published on Thursday.

The rise in drilling costs has barely started to reverse the previous 34 per cent decline reported between March 2014 and November 2016, but it does mark an important turning point in the oilfield services costs cycle.

Drilling costs have been rising year-on-year since March and in June were almost 3 per cent higher than in the corresponding month a year earlier.

Services costs are cyclical and follow changes in the rig count with a lag of a few months, but so far cost increases have been very modest compared with the resurgence in drilling activity.

Services costs are cyclical and follow changes in the rig count with a lag of a few months, but so far cost increases have been very modest compared with the resurgence in drilling activity.

The number of active rigs has more than doubled over the last year, according to oilfield services company Baker Hughes, while costs have risen by less than 3 per cent.

The number of active rigs has more than doubled over the last year, according to oilfield services company Baker Hughes, while costs have risen by less than 3 per cent.

Drilling costs have remained low as rig owners have engaged in deep discounting to win contracts following the worst slump for more than a generation.

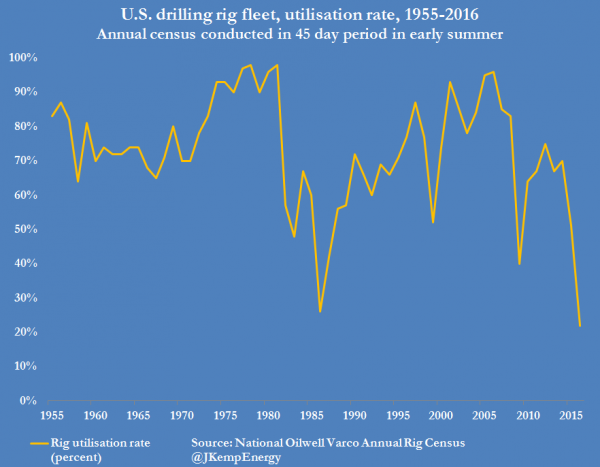

In the early summer of 2016, there were 2,100 rigs available for use in the United States, but just 455 were operating, according to an annual census conducted by National Oilwell Varco (NOV).

NOV defines a rig as “available” as one that is currently active or ready to drill without significant capital expenditure (“63rd Annual Rig Census”, NOV, 2016).

NOV defines a rig as “available” as one that is currently active or ready to drill without significant capital expenditure (“63rd Annual Rig Census”, NOV, 2016).

The utilisation rate of 22 per cent was the lowest in over six decades, and down from 51 per cent in 2015 and 70 per cent in 2014.

To be considered still available, a land rig must not have been idle for more than three years, or five in the case of offshore units.

To be considered still available, a land rig must not have been idle for more than three years, or five in the case of offshore units.

Badly damaged rigs, those which have been cannibalized for spare parts, and any in long-term storage are excluded.

The large number of idled rigs last year sparked fierce competition among operators and intense discounting to secure contracts.

As a result, exploration and production companies were able to lock in very favourable drilling rates for 2017 in the second half of 2016.

But the drilling boom has significantly reduced the number of idle rigs and given rig contractors more pricing power.

The number of active rigs has climbed from a cycle low of just 404 at the end of May 2016 to 952 in early July 2017.

The utilisation rate is now well over 40 per cent, which is still low by historic standards, but no longer at emergency levels.

The rigs which are still idle are mostly older, less powerful, less sophisticated and likely less productive.

As the rig count continues to increase, and contracts negotiated during 2016 expire, drilling firms are likely to push for significant price increases.

Oilfield services costs are therefore set to rise in the second half of 2017 and especially in 2018 unless the drilling boom slows.

Related column:

“Drilling costs rise as U.S. oil, gas activity picks up”, Reuters, April 26

Editing by David Evans

John Kemp is a Reuters market analyst. The views expressed are his own.

Subscribe

If you enjoyed this article, subscribe to receive more just like it.